Embedded Finance — Is It Taking Over the Fintech Market?

Nowadays, almost everybody interacts with financial services each day, in some way or another. We transfer money to our friends, pay for products and services online, purchase various subscriptions, and so on. People spend, borrow, earn and save all the time.

But times are changing, and even basic financial operations now require more complex services and high-tech solutions. This level of integration and interaction with financial services was unimaginable twenty, even ten, years ago. Now, embedded finance is steadily taking over and establishing its own place in our lives.

Embedded finance is, of course, a relatively new concept. Basically, it allows the use and implementation of financial services for a company that is not itself a financial organization. As an example, think of a retail store chain that, for instance, provides fast and simple lending services such as a ‘buy now, pay later’ scheme. This is, of course, a consumer-led benefit, but what about businesses? Well, the same company, by using special fintech solutions developed by a fintech service provider such as Whillet, can implement a more equal and efficient distribution of money to pay, say, for a food delivery — one payment being instantly divided into small transfers, each dedicated to various stages of the delivery process.

So you see, embedded finance services can create enormous opportunities for new types of doing business, whether for the giants of the market like Facebook, Lyft, Uber, and the like, or for fresh-faced start-ups. Once, creating an innovative company from scratch, while having little early growth capital, was almost impossible. Now, with the option of having all the previous difficult tasks of creating, upbringing and managing an innovative, fast-growing company, the process is totally simplified. No more establishing it from scratch requiring massive funding. Market barriers of entry have already been lowered and will be significantly so in the near future. According to 2022 Statista research, the number of fintech start-ups in the Americas nearly doubled in 2018-2021. Therefore, it’s true to say that embedded finance is one of the latest great achievements in the world of business and commerce.

How was this revolutionary new solution developed?

Well, the process has three main stages:

- Financial services are dominated by brick-and-mortar organizations like banks, investment companies, and so forth in a simple and somewhat inflexible order. They have rather limited use and high entry barriers. Who really needs to go to the bank every day to draw a check, make a transfer or lend some money? Moreover, the accessibility of financial services was strictly tied to the bank’s specific credit policy. Access to information about those processes and solutions has strict limitations, and their handling simply requires more time and resources.

- The gradual decoupling of major financial organizations generated a huge number of first-wave fintech organizations that began using cutting-edge innovation to provide various financial services on top of the usual banking service. Companies rapidly emerge and become major players themselves. E-commerce is on the rise, but this range of utilities is accessible only online without direct connection to offline services and businesses. Restrictions on data are also being lifted with merchants now using it to improve their own business processes and decision-making fully online, all in a matter of seconds.

- Financial services inevitably democratize and become embedded with perspectives of usage being almost boundless, always pushed by start-ups. Such services can now be used and provided not only by specific fintech companies but also by non-financial entities — and when you think about it, this includes almost every single type of company. More and more customers will result due to the rapid emergence and widening usage of technological advancements, especially the digitally-based. Online services can finally form a synergy with offline firms, providing them with fintech solutions integrated (embedded) into companies’ own ecosystems and interfaces.

There are three vital functions performed by financial services in general and by embedded finance in particular. For an economy to thrive and society to develop normally, businesses need to operate with institutions that provide these services. But times are changing and organizations should not only use the options available to them but integrate and implement them. Those three essential functions are:

- Storing or transferring money (or any other currency) for everyday payments/transactions.

It constitutes an essential part of the present-day economy. It is one of the most widely used embedded solutions — even social networks like Facebook, Lyft or WeChat develop their own payment services. Food delivery services and taxi firms are typical examples.

- Storing or transferring any value in a timely fashion.

This is about loans, credits and investments — those things that change their value over time. Traditionally, this was the domain of major banking organizations but now, with embedded financial services, almost any type of business — including retail, health and education — can put in place facilities such as PoS lending or ‘Buy now, Pay later’ (BNPL). Consider for a moment all those installment plans provided by electrical retailers for appliances or garment purchases in clothing stores. Today, they require practically little or no paperwork so there is no need to worry about the credit score checking process. But the customer doesn’t have to interact with lots of organizations for approval, usually just the one company.

- The management and handling of chance, bad luck or chaos scenarios.

With the emergence of embedded finance and the widening of technical integration, there are more and more opportunities to simplify the process of getting insurance in almost any area of human activity or business. Whilst it’s slightly different from other embedded services, it makes it possible for any third-party product, service provider or developer in any industry to effortlessly incorporate innovative insurance solutions into offers for clients. Insurers gain access to new customer data and can perform real-time risk assessments. For example, smartphone distributors can include insurance packages as an option for their customers during the online purchasing process.

So the functions described above constitute the three main sectors in which embedded finance is currently developing but is not limited to them. Namely, payments and transactions, lending, and insurance.

Now let’s take a closer look at the biggest growth area — embedded banking. Together with payment services, it is a telling example of popular technology that is currently at the forefront of embedded services development. It’s important to note that embedded banking includes almost all the services just mentioned.

Embedded banking is the branch of fintech where bank-like services are provided by organizations and companies that, traditionally, do not necessarily deal with investments and finance. It replaces the traditional bank account. With one unified service provided by a single platform or organization, you can invest, apply for loans and credits, issue and manage credit/debit cards, or deal with your payments. As you might see, this includes embedded payments solutions in some way, too. What this approach does is offer clients a consistent financial experience.

Embedded banking makes processes more productive, less stressful and fewer resource costs. They are significantly more practical and easy to use compared with typical banking. With these technologies, it is easier for companies to build their own financial ecosystem for employees or customers without the need to invest billions of dollars on creating and managing the infrastructure, licensing and all the other disadvantages. They can simply buy it ‘as-a-service’ from another company — like Whillet. Remember, back in 2019, Apple released its own credit card with a package of personal financial management instruments.

So you see, everything mentioned above is not just lots of words full of empty pie in the sky predictions and possibilities, it’s happening right now — a living and thriving market with billions of dollars invested each year and going strong.

Let’s have a look at some graphs and numbers:

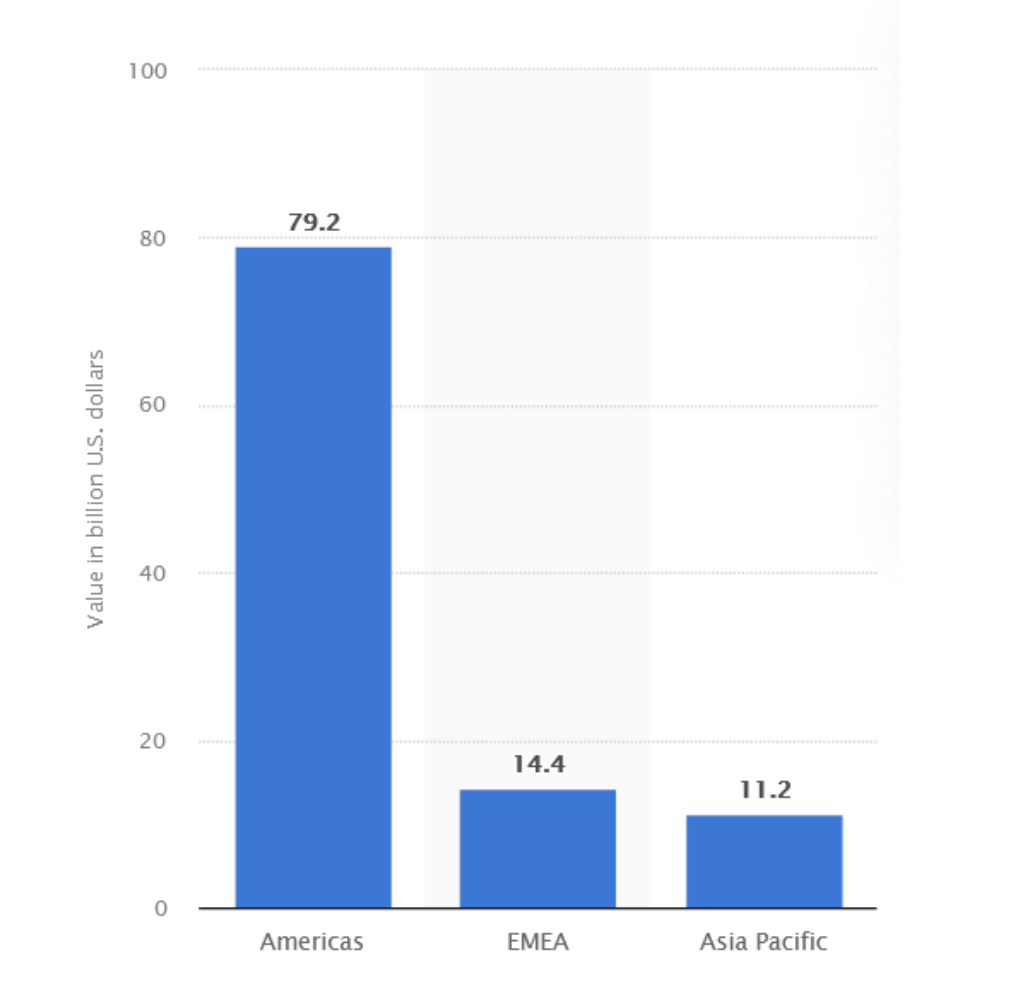

According to a 2022 Statista review, the total value of the investment in fintech in the Americas region just in 2020 almost reached a staggering $80 billion US, with $105 billion invested worldwide:

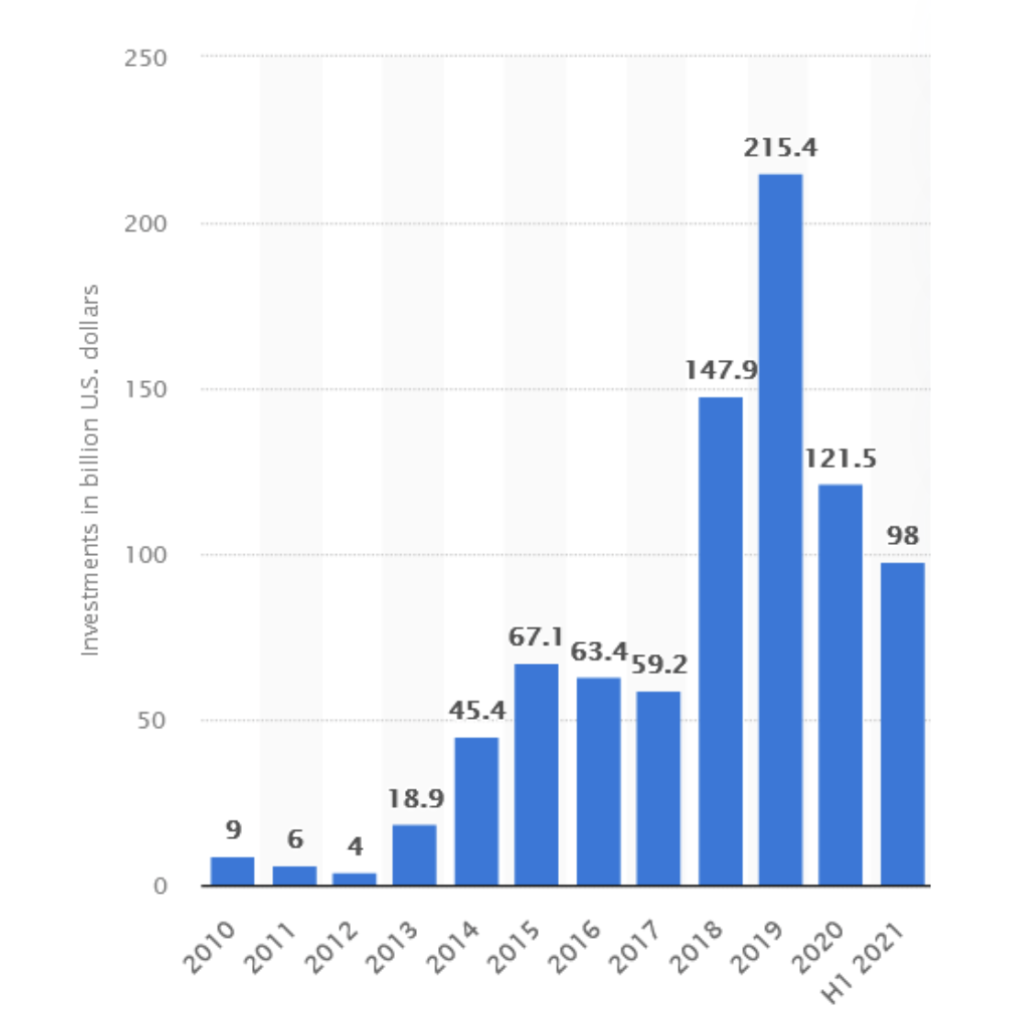

And only in H1 2021 alone worldwide investments in fintech totalled 98 billion US dollars:

What’s more convincing, venture funds did not stay idle either — an incredible sum $4.2 billion dollars was invested in the first nine months of 2021 alone. That’s a huge increase from $1.5 billion in 2020 and $0.4 billion in 2018:

Conclusion

As we’ve seen, embedding has rapidly become the main development trend for businesses worldwide, with investments continuing to be sustained. What previously was the area of big traditional financial business domination now becomes the main feature of virtually every type of company, with greater global access to finance and creating many opportunities for start-ups, while revolutionizing both customer and business experience.

Whillet provides your business with flexible, high-quality API-based instruments, which can help your business expand the field of services offered by the company in the sphere of embedded finance. You can implement financial services under your own brand and fully customize your products according to your company’s business specifics.